Market Update 8/9/21

By Jason Teed

The major U.S. stock market indexes ended higher once again last week, with several indexes flirting with all-time highs. The NASDAQ Composite turned in the best performance with a 1.11% gain, the Russell 2000 rose 0.97%, the S&P 500 was up 0.94%, and the Dow Jones Industrial Average gained 0.78%. The 10-year Treasury bond yield rose 7 basis points to 1.30%, taking bonds slightly down for the week. Spot gold closed the week at $1,763, down 2.82%.

Only one sector was down last week: Consumer Staples fell 0.55%. Financials and Utility stocks performed the best last week, up 3.56% and 2.28%, respectively.

Stocks

The equity markets were up last week. Riskier segments of the equity markets tended to perform the best, though Utility stocks were a strong outlier.

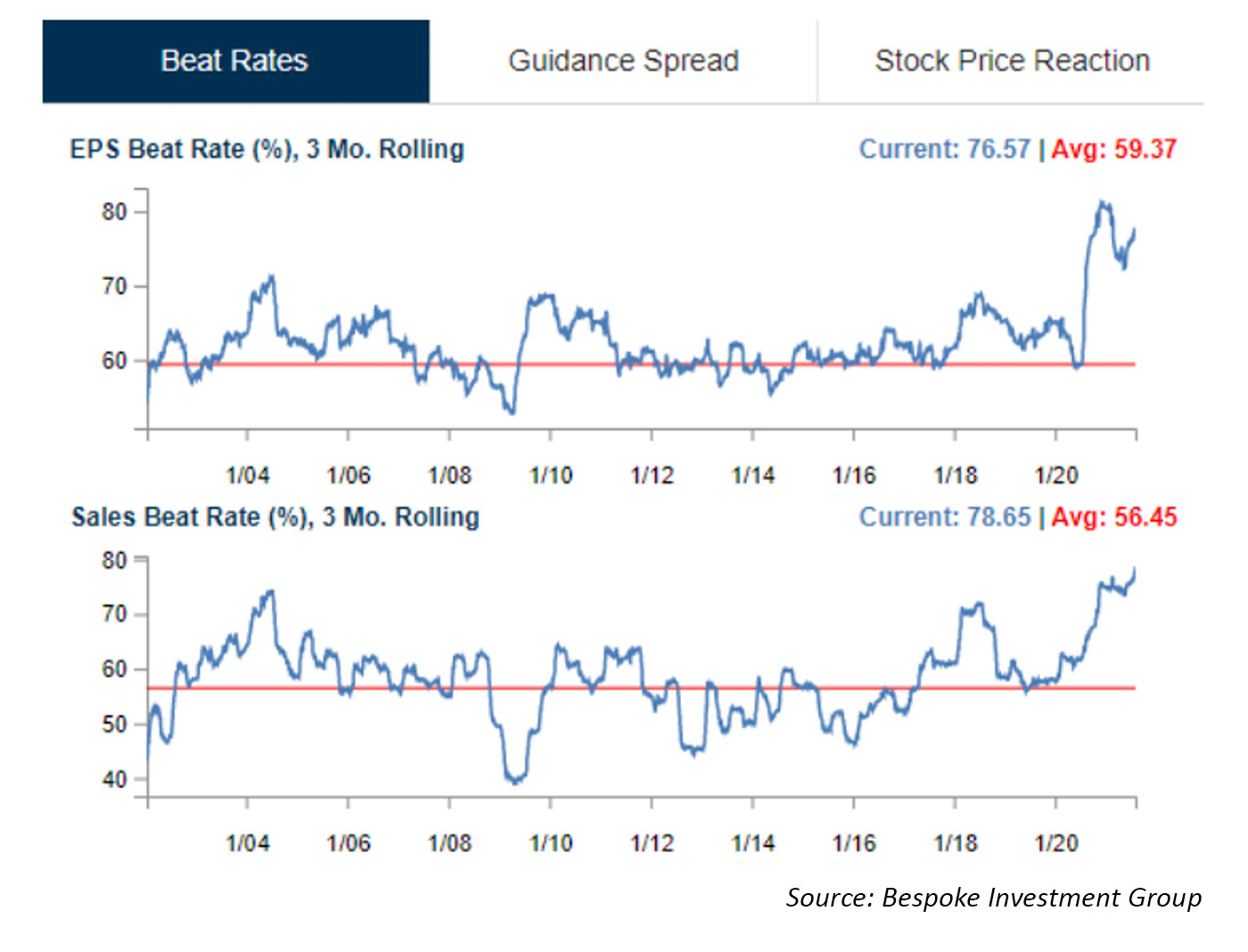

The strongest tailwind for stocks has been earnings. Most companies have surprised with exceptionally high earnings. The earnings beat rate is currently around 80%. Stock reactions to these reports have been more muted than they have been historically, but that may be because the market has already anticipated these earnings.

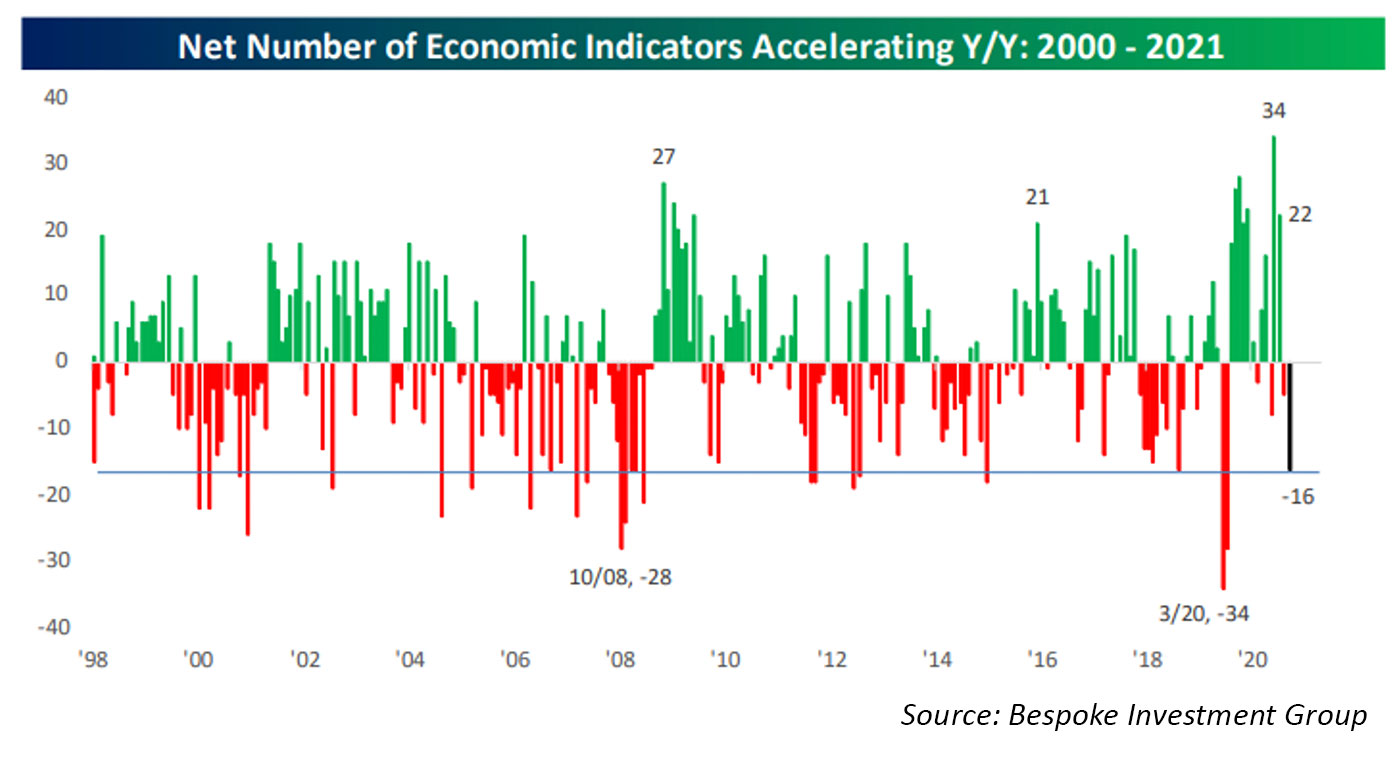

Economic indicators remain mixed, although historically favorable. Last month’s report was the lowest reporting that we’ve seen since the 2020 bear market, though that is after several exceptionally strong weeks. Mean reversion between high levels is expected. As yet, these readings are no cause for alarm.

Additionally, productive assets such as copper and oil have come off their yearly highs, suggesting that the market is no longer pricing in continued recovery. However, it doesn’t appear to be pricing in any major reduction in demand either.

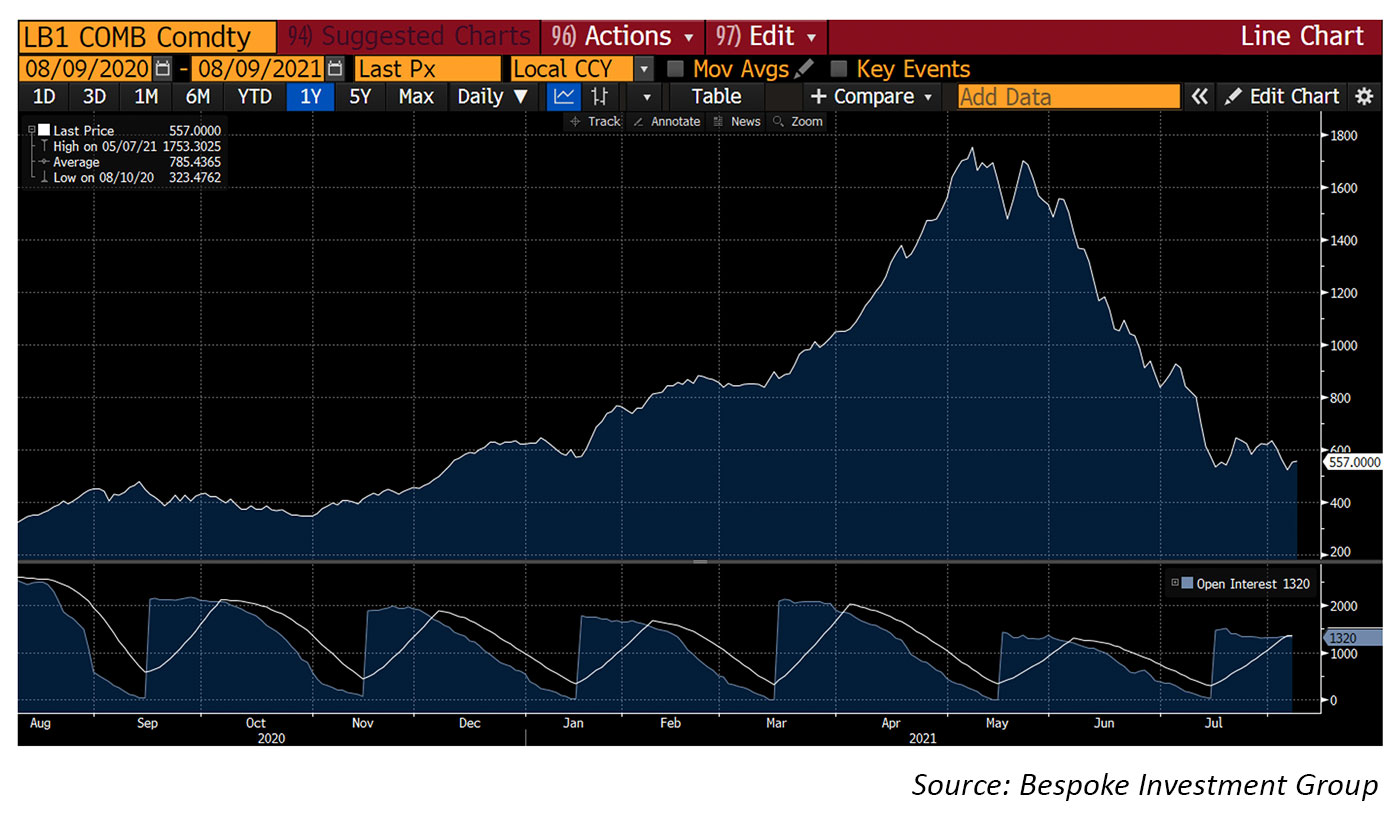

While lumber appears to be normalizing, having significantly fallen from its previous highs, it remains high versus historical levels. This is challenging for the market as a whole. The commodity topped out at nearly $1,800 per contract. It is now trading at $557, which, while seemingly no longer in bubble territory, remains a headwind for the economy as a whole. This leveling off has also not yet translated to savings for consumers. Builders still have to contend with commodity shortages and a lack of skilled labor, both of which are expected to continue in the intermediate term.

Supply disruption and a labor shortage could also continue to remain headwinds for U.S. equities. The expiration of supplemental unemployment benefits in addition to the start of the 2021–2022 school year could see an increase in labor supply, which could help address both challenges in the coming months.

While the economy has some issues to overcome, corporate earnings momentum has given equities a boost that may keep the asset elevated through those near-term challenges.

Bonds

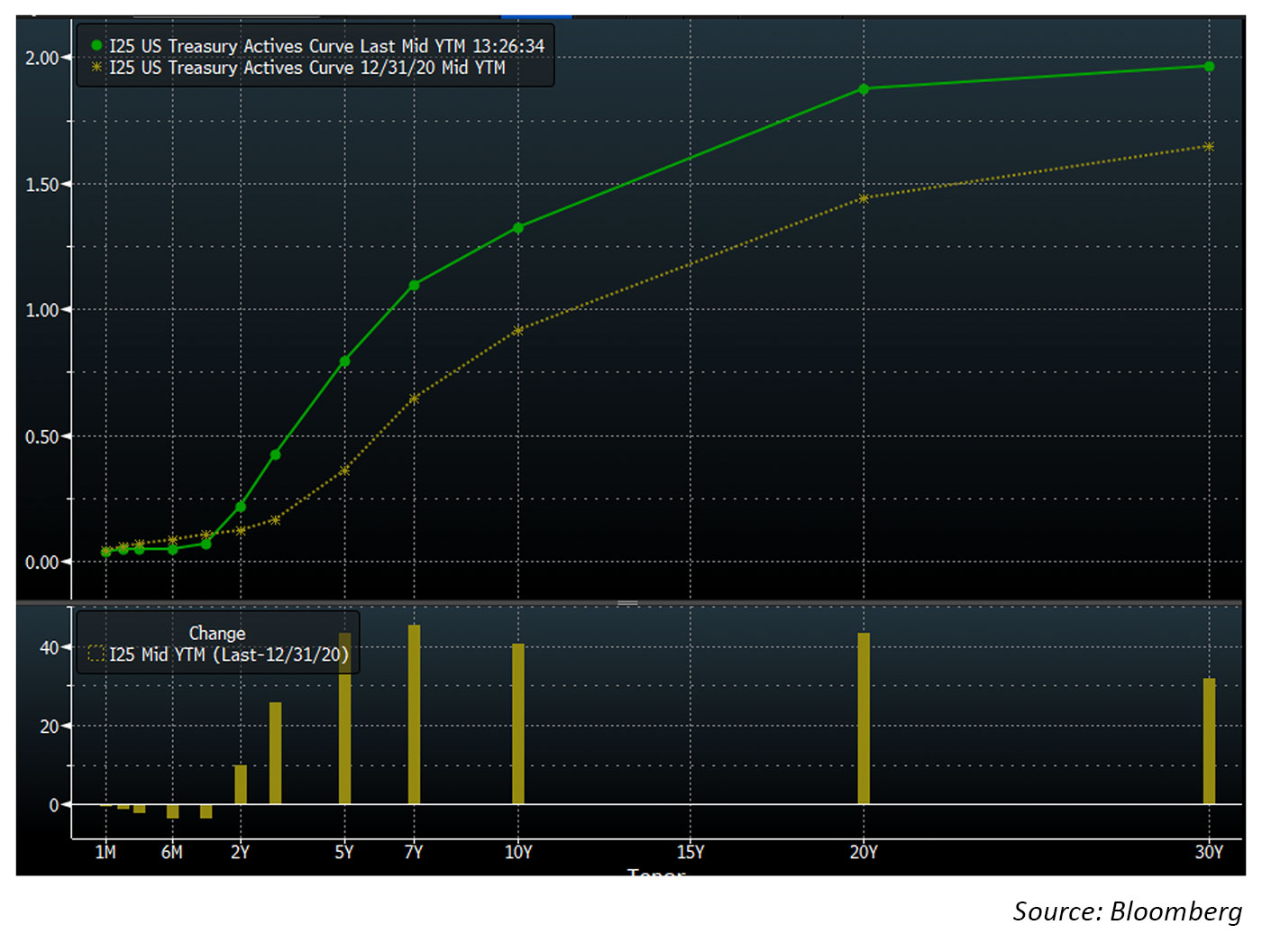

Treasury yields decreased once again as yields continue to ease. The 10-year Treasury climbed to 1.30% last week after having fallen significantly from this year’s previous highs.

Yields are still historically low. Credit spreads fell for the week and term spreads increased, both indicating healthy economic expectations going forward. Overall, long-term Treasurys underperformed high-yield bonds, and longer-term bonds underperformed shorter-term bonds.

Expectations for the intermediate term have increased—but not as quickly as recently forecast. This may drive investors to seek yield and performance in other asset classes.

Gold

Spot gold experienced a “flash crash” over the weekend during Asian market hours. Other safe-haven assets, such as long-term Treasurys, underperformed, primarily due to a pause in decreasing interest rates.

Recent strong economic reports have put pressure on the metal along with other safe-haven assets, though the Federal Reserve is expected to keep interest rates low in the short term. Inflation has rebounded but its rise is slowing, and the nature of that rebound is likely to keep the Fed standing pat on interest rates for now.

Flexible Plan Investments (FPI) is the subadvisor to the only U.S. gold mutual fund, The Gold Bullion Strategy Fund (QGLDX), designed at its introduction nine years ago to track the daily price changes in the precious metal.

The indicators

Our Political Seasonality Index started out last week fully exposed to the market. It exited on Tuesday’s close and remained there for the rest of the week. (Our QFC Political Seasonality Index is available post-login in our Weekly Performance Report section under the Quantified Fund Credit category.) The very short-term-oriented QFC S&P Pattern Recognition strategy’s equity exposure was 2X long for the week.

Our intermediate-term tactical strategies are uniformly positive, although to varying degrees. The Volatility Adjusted NASDAQ (VAN) strategy started the week with 140% exposure to the NASDAQ. It increased exposure to 160% on Tuesday’s close, to 180% on Wednesday’s close, to 200% on Thursday’s close, and remained there to begin this week. The Systematic Advantage (SA) strategy was 90% exposed to the market last week, changing to 120% exposure to begin this week. Our Classic strategy is in a fully invested position, and our QFC Self-adjusting Trend Following (QSTF) strategy was 200% long for the week. VAN, SA, and QSTF can all employ leverage—hence the investment positions may at times be more than 100%.

Flexible Plan’s Growth and Inflation measure, one of our Market Regime Indicators, shows that we remain in a Normal economic environment stage (meaning a positive monthly change in the inflation rate and positive monthly GDP reading). Historically, a Normal environment has occurred 60% of the time since 2003 and has been a positive regime state for stocks, bonds, and gold. Gold tends to outpace both stocks and bonds on an annualized return basis in a Normal environment but also carries a substantial risk of a downturn in this stage. From a risk-adjusted perspective, Normal is one of the best stages for stocks, with limited downside.

Our S&P volatility regime is registering a High and Rising reading, which favors equities over gold and then bonds from an annualized return standpoint. The combination has occurred 23% of the time since 2000. It is a stage of average returns for equities and gold, but lower-than-average returns for bonds.